Published on: 08/27/2021 • 5 min read

Avidian Report – Could a Value Tilt Be Appropriate in Portfolios Today?

INSIDE THIS EDITION:

Could a value tilt be appropriate in portfolios today?

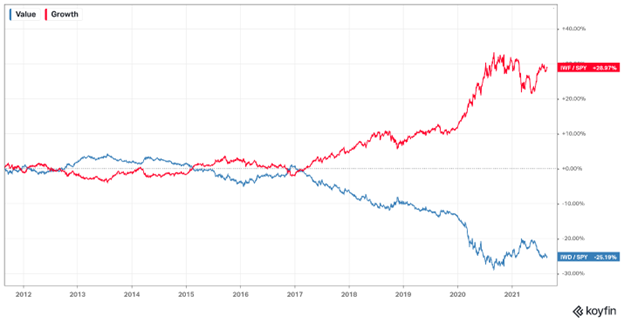

Over the last several quarters, there has been a debate about whether the value will ever return to prominence overgrowth in equity markets. This is despite signs of life from so-called value stocks, which for over a decade of underperformed growth stocks.

Today, we continue to witness an environment where growth continues to be the flavor de jour for stock market investors, but we question whether a sustained change in leadership may be afoot. This week’s report investigates growth vs. value and determines whether things may start looking a bit brighter for value investors.

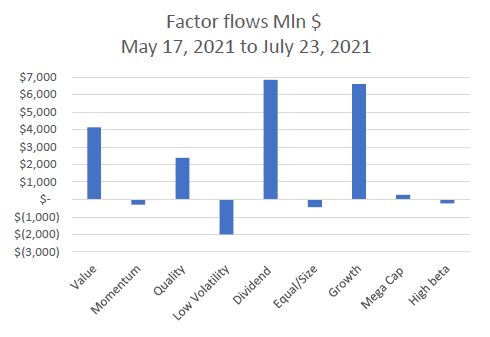

However, before getting into that discussion, it is worth looking at data related to fund flows and what it may be signaling to stock investors. In the chart below, we see fund flows into ETFs tied to different factors. Despite a slowdown in inflows to value-oriented ETFs, investor interest in the value factor remains.

All of this is despite the relative underperformance that value and value managers have generated relative to growth over the last decade.

For some context, there were approximately $35B of inflows to value-based ETFs through May 17. Since then, we have seen a slowdown, but this is attributable to investor interest in low volatility strategies and growth-focused equities buoyed by uncertainty surrounding the economic reopening.

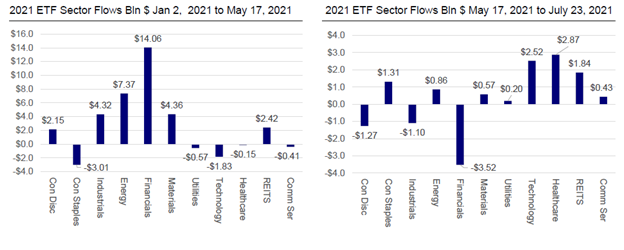

This fact becomes apparent when looking at ETF sector inflows shown in the two charts below. Since May 17, what we think about as value sectors like banks have seen outflows, while growth sectors like technology have seen strong inflows. This also highlights investors’ preference for more defensive stocks over the last couple of months as growth worries periodically enter the headlines.

However, eventually, value will have its day. It may not be today, and it may not be tomorrow. But value should shine once again. And this is just one reason why we advocate exposure to both growth and value factors in your portfolio. After all, most people like a bargain, and at the core, this is what the value factor represents for investors – a bargain relative to intrinsic value. Not only does the value factor represent a sale, but it also does so while adding diversification through a factor that historically has shown that it can outperform. But perhaps most importantly, the value factor represents an opportunity on a relative valuation basis.

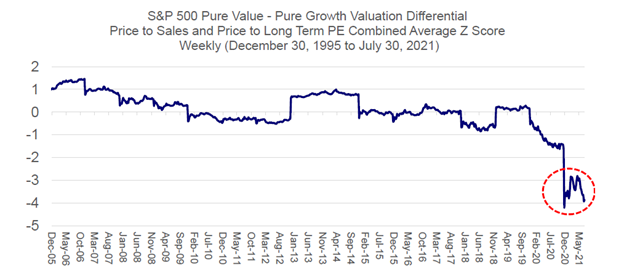

As the chart below shows, the spread in valuation between S&P 500 Value Index and the S&P 500 Growth Index is at its widest level going back 15 years. This is similar to the story told by long-term PE ratios and price to sales ratios for both value and growth. The key takeaway is that value factor stocks are as cheap as they have been in a long, long time.

And for purist growth investors, we have some good news if you typically resist the value slant. Namely, value might represent more growth than initially meets the eye.

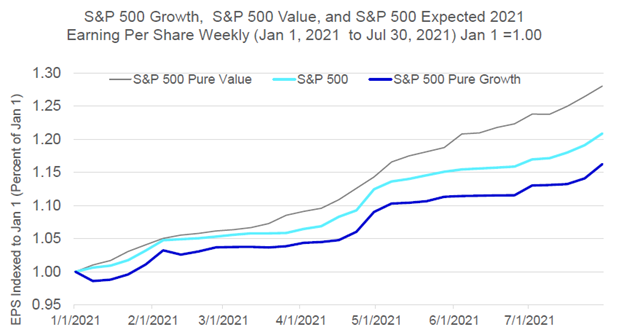

Take, for example, what we see as it relates to earnings revisions.

As the chart above shows, the S&P 500 Pure Value Index has produced more positive earnings growth than both the S&P 500 and the S&P 500 Pure Growth Index. There is a strong possibility that this persists not only through the remainder of 2021 but possibly even into next year, albeit perhaps in a less pronounced fashion.

This makes value attractive not only for the value crowd but also for the growth investor.

Lastly, we want to address the idea that we are perhaps past peak economic growth (or very close to it) and how that fits with the conventional wisdom that value does better relative to growth only when the economy is in its early growth phase.

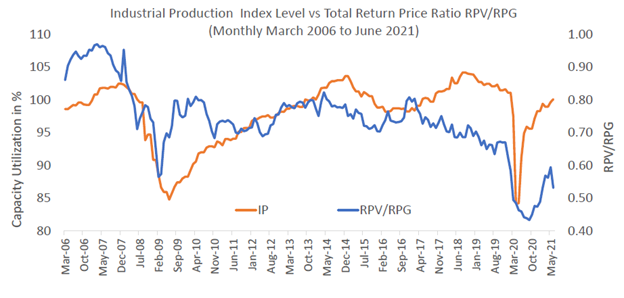

To address that, let’s look at industrial production as a proxy for economic activity. Value outperformance overgrowth has historically correlated well to industrial production. However, where we sit right now, industrial production still sits below its pre-pandemic peak, and value outperformance overgrowth ratios appear to have a spread to close. This seems to lend some credence to our view that having a slight value tilt at this stage could make sense in many equity-focused portfolios.

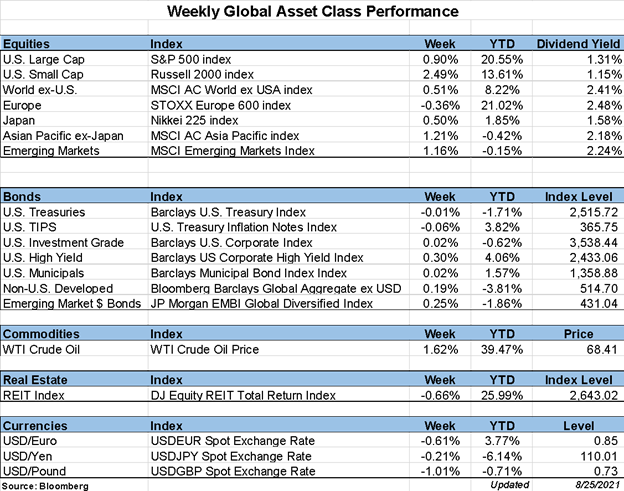

Weekly Global Asset Class Performance

Please read important disclosures here

Get Avidian's free market report in your inbox

Schedule a conversation

Curious about where you stand today? Schedule a meeting with our team and put your portfolio to the test.*