Published on: 04/30/2021 • 5 min read

Avidian Report – How Much Longer Might The Fed Hold Rates Near Zero?

INSIDE THIS EDITION:

How Much Longer Might The Fed Hold Rates Near Zero?

The Fed funds rate is the target interest rate set by the Federal Open Market Committee (FOMC) at which commercial banks borrow and lend their excess reserves to each other and can have a meaningful impact on short-term rates on things like consumer loans. This week, the Fed issued a statement updating us on their stance over target interest rates. The biggest takeaway was that despite strong economic improvements in the US, the central bank would remain accommodative as in their assessment. The economy still faces considerable risks, especially related to the employment picture, which shows more than 8M fewer people working today than during pre-pandemic levels.

Of course, we do question how many of these folks would be back to work if it were not for stimulus checks and other support mechanisms that, in some ways, have disincentivized some people from returning to work.

Regardless, we think the Fed is mainly sticking to their game plan and adhering to the script they laid out when they updated their policy framework in September 2020.

Under the new framework, it appeared the Fed would remain committed to accommodative policy. The only way that would shift would be if we saw a monumental change to economic conditions or reemergence of dysfunction in securities markets, neither of which we have seen.

Selected Assets of the Federal Reserve

Granted, we have observed an improvement in economic conditions, but one that remains in some ways incomplete.

And we believe it is this that will keep the Fed accommodative for the near-term. However, we think the Fed’s pressure to raise rates may increase as we get into 2022, especially as it appears that inflation pressures in some parts of the economy are building. If we observe the Federal Reserve Dot Plot, we now have three more Fed officials projecting a rate hike in 2022 than we had during the last update.

Federal Reserve Dots Plot of Rate Expectations

For investors, we believe this means that portfolios should be positioned for bumps to inflation by including a small allocation to inflation hedging securities. We have been discussing this for quite a while but believe the window may be closing before pent-up demand starts to have an inflationary impact on headline inflation numbers. While we are somewhat conflicted on the durability of the inflationary episode ahead, we think considering an exposure to securities like TIPS on the fixed income side of the portfolio and real assets like real estate, infrastructure, and commodities sense from a portfolio construction standpoint.

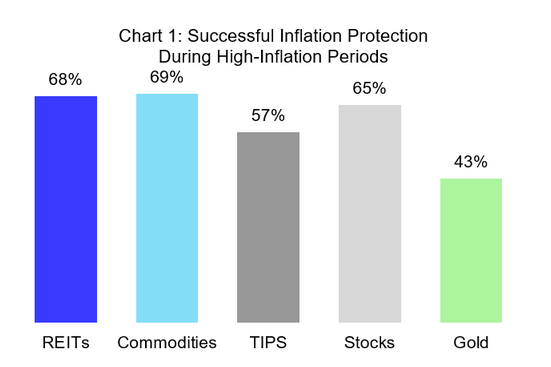

As the chart below shows, commodities and REITs have historically provided solid inflation protection with total returns running above inflation in nearly 70% of high inflation periods, defined in this case as 6-month periods when inflation runs ahead of the long-term median.

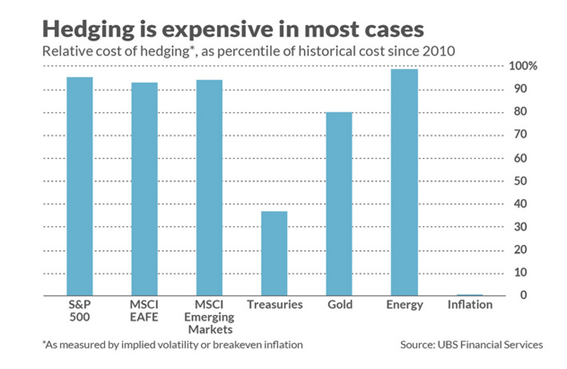

For investors not currently holding inflation hedging asset classes, there is an upshot. Namely, putting on the exposure today remains very inexpensive relative to the cost of hedging other risks a portfolio may face over a full economic cycle. While some of these asset classes have shown the strong performance of late, many are still favorably valued, and history has indeed demonstrated that they can effectively protect purchasing power and help ensure that financial plans remain on track.

If your advisor is not including some of these asset classes in your portfolio, you should be asking why. After all, for investors to be successful over time, they must hold portfolios built not for the present but for the wide range of possible outcomes in the future.

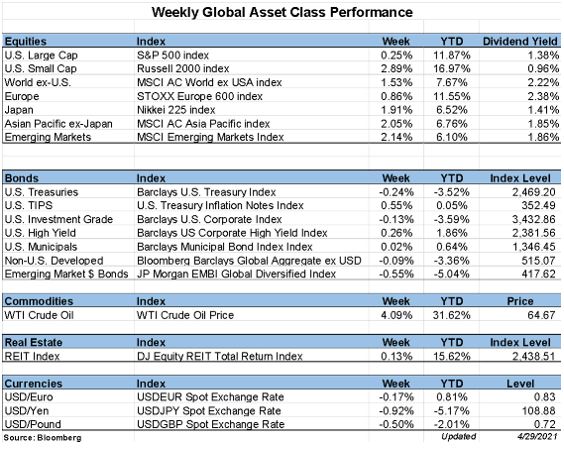

Weekly Global Asset Class Performance

Please read important disclosures here

Get Avidian's free market report in your inbox

Schedule a conversation

Curious about where you stand today? Schedule a meeting with our team and put your portfolio to the test.*