Published on: 06/25/2021 • 5 min read

Avidian Report – Where Do Equities Go From Here?

INSIDE THIS EDITION:

Where Do Equities Go From Here?

June 2021 Update – FPA Tax and Estate Planning Knowledge Circle

Over the last month, domestic stocks as measured by the S&P 500 have continued to grind higher. This despite a pull-back on the heels of the Fed statement last week. If you did not catch it last week, investors viewed the Fed’s comments as marginally hawkish and led some investors to get concerned about potential interest rate increases. Undoubtedly, this led to the unwinding of inflation trades that many traders had put on over the preceding weeks.

However, we continue to think this was largely an overreaction. The Fed has shown the ability to talk up and talk down both inflation and potential policy moves. We do not expect this to change anytime soon. So, while a lot of investor attention has been on Fed policy statements and other comments from Fed governors since the meeting last week, we have been observing other data that might warrant a move away from a more neutral stance. However, we still have not seen a reason to do so just yet.

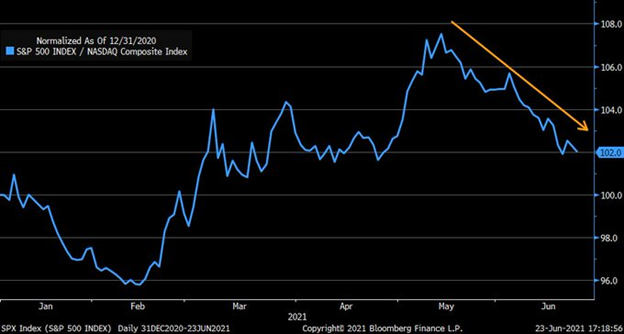

After all, since mid-May, NASDAQ has seen a significant increase in strength relative to the S&P 500. This is very similar to what we saw between mid-February and early March. If we look at index leadership between the S&P 500 and NASDAQ since the start of the year, the S&P 500 leads the way, but by a narrow margin. We believe this narrow differential in performance could signal investors simply trying to figure out which direction the market is likely to move in and which sectors will lead the way.

There are simply many forces at play that might tilt the scales in one direction or another. And this is one reason we currently advocate for more neutral portfolio positioning blended with some tactical positions that could perform well under various scenarios. This positioning should provide the right balance of return potential and flexibility. While we have seen an unwind of some inflation hedges, we think this is the wrong move. We view them as an insurance policy in the event that higher inflation readings stick around for a while longer than expected, especially in light of a new bipartisan infrastructure deal now in place. With that, it looks unlikely in the short-term that we will run into any significant headwinds for a continued march higher for the broad indices and instead may see further support for a continuation of the transitory inflation narrative that the Fed has highlighted numerous times. How long it lasts, of course, remains to be seen.

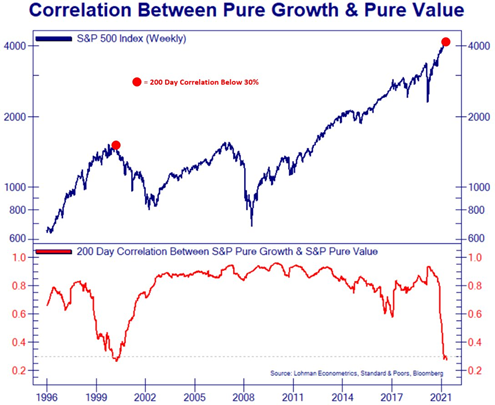

Taking a deeper look at market internals, we have also seen an interesting development related to technology shares that do not show profits. Namely, they have outperformed the S&P 500 by a meaningful 10%, the widest performance spread since January of this year. We saw a spread at similar levels for unprofitable tech shares over the S&P 500 and a subsequent reversal where the broader market outperformed from February to May. Like back then, this may indicate the tug-of-war that is currently occurring between growth and value stocks.

While this may continue for some time, our preference is to remain reasonably balanced in portfolios but with a slight value tilt. This is appropriate considering the 200-day correlations between growth and value factors that have now dropped to approximately 0.30. By usual standards, this is low, with the last drop of this magnitude occurring at the front end of the dot-com crash.

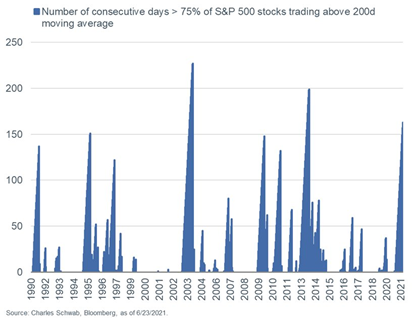

By no means are we saying that we will see a repeat of what happened then, especially when we consider that this year, we see a long streak of days where three-quarters of the S&P 500 trades above their 200-day moving averages.

In our view, this is very constructive for the broad market, with technicals still flashing bullish signals and the infrastructure agreement likely adding optimism for a continuation of the current uptrend.

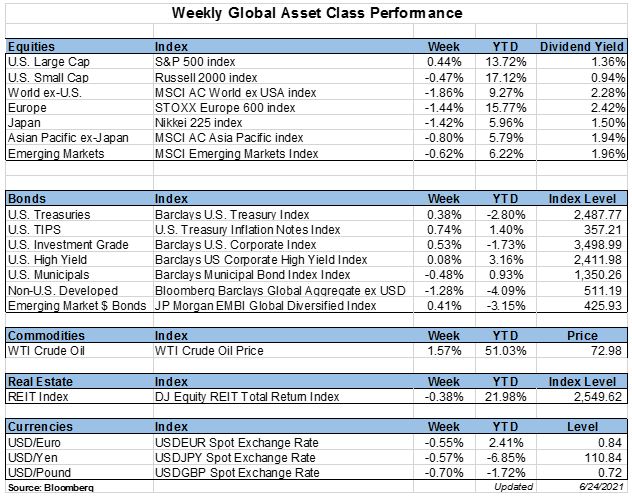

Weekly Global Asset Class Performance

June 2021 Update – FPA Tax and Estate Planning Knowledge Circle

Written by Scott Bishop, MBA, CPA/PFS, CFP®

Since the election last November, I have been talking with experts and writing articles on potential income and estate tax changes under the new Biden Administration and Democratic Congressional majorities. Several of these articles are listed below.

Early in the new year, I wrote an article called Key Estate and Income Tax Planning Takeaways from the “Blue Wave” Democratic Victories based on my interview of and discussions with Marvin Blum, JD/CPA of the Blum Firm.

Click Here to Read the Entire Article

Please read important disclosures here

Get Avidian's free market report in your inbox

Schedule a conversation

Curious about where you stand today? Schedule a meeting with our team and put your portfolio to the test.*